macropulse

The Macro Middleware: Machine-readable alpha via API.

G

@gabrielveron134

Details

- Follow on

- @macropulslv

- Categories

- Analytics & MonitoringFintech

- Target Audience

- Data ScientistsDevelopersBackend Developers

Discovery signals

How AI and people discover macropulse on PeerPush

About macropulse

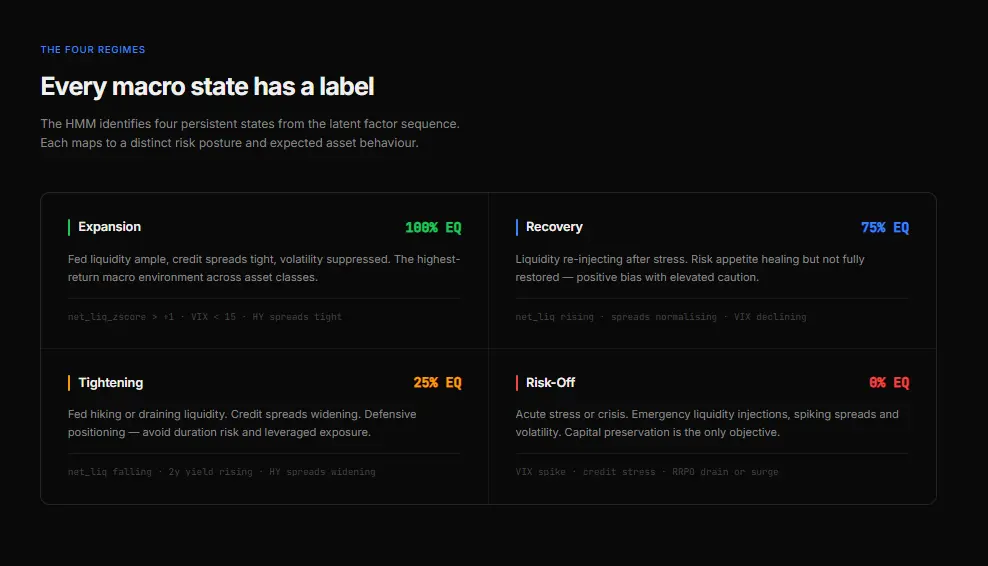

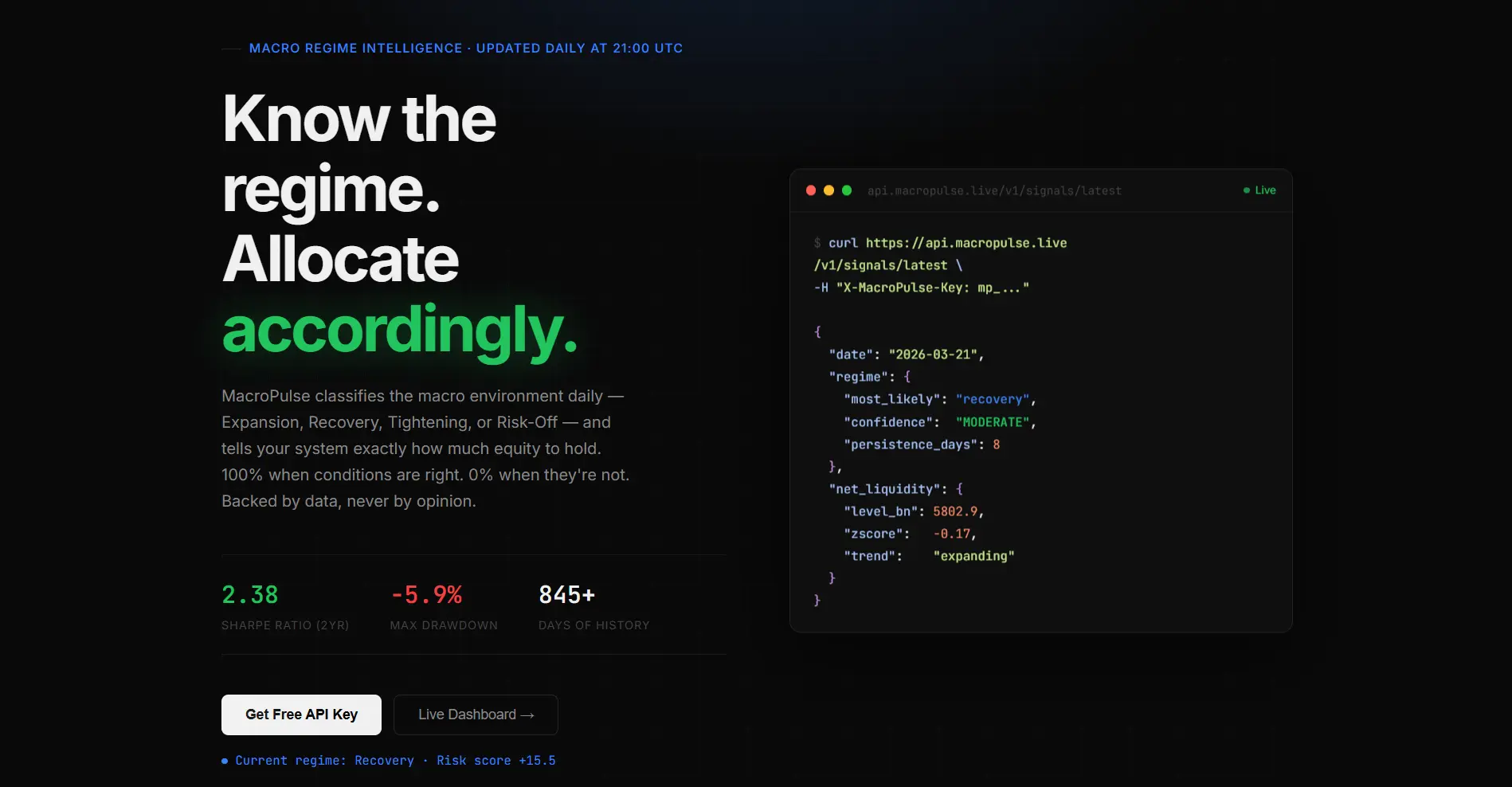

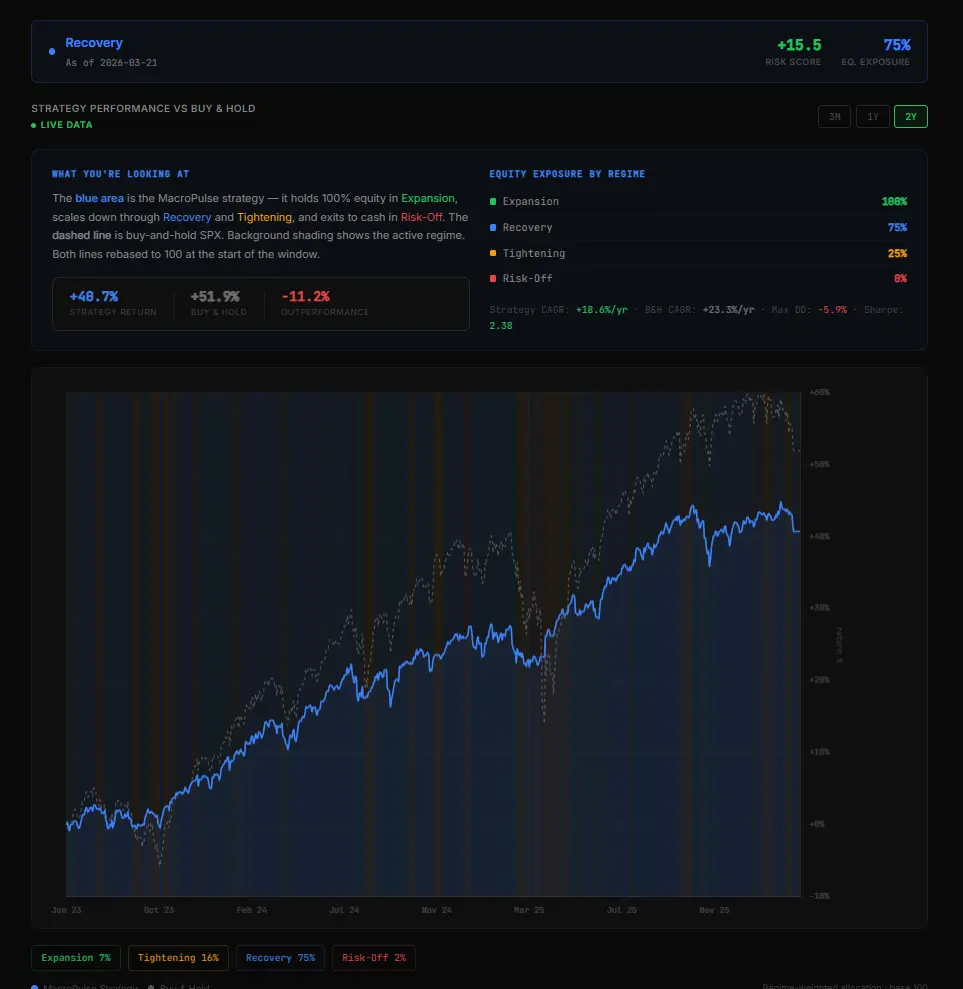

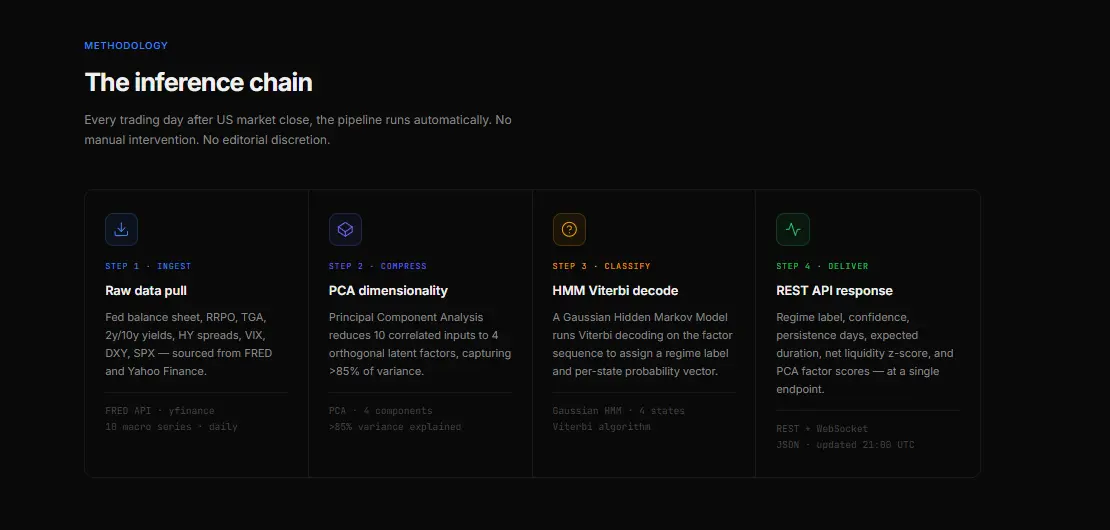

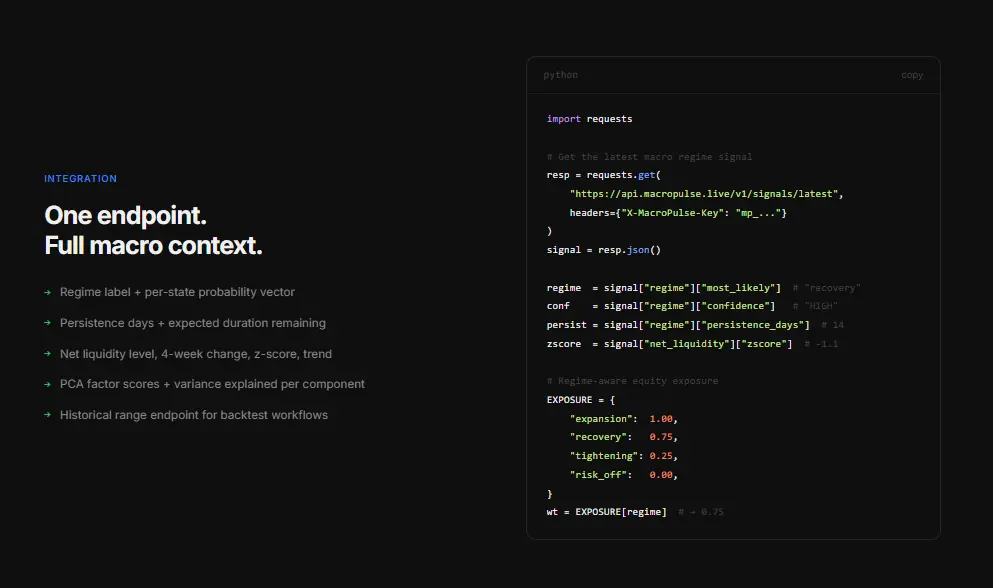

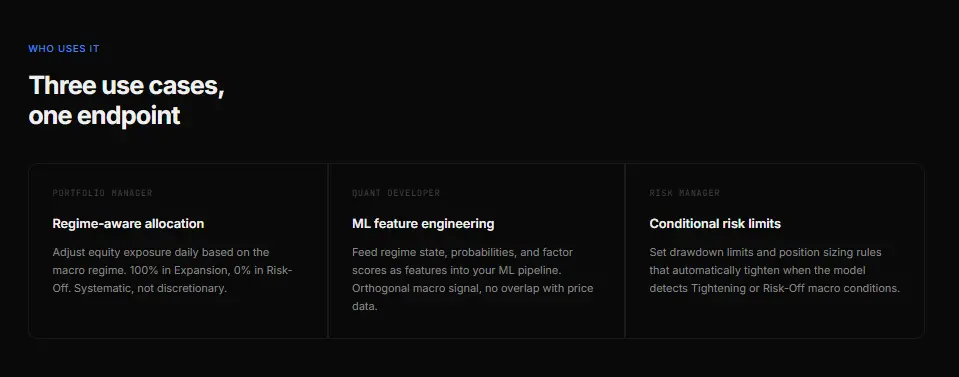

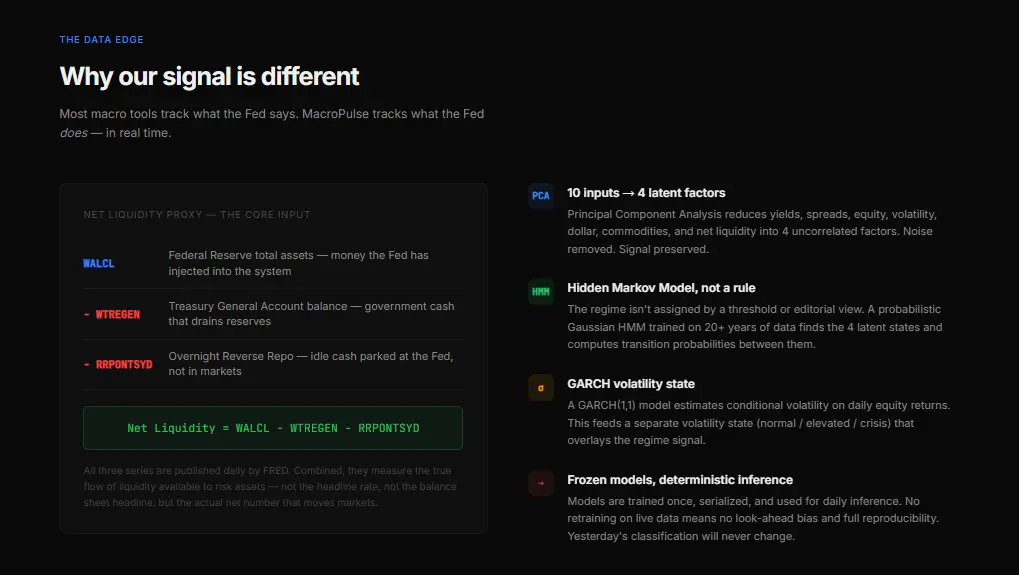

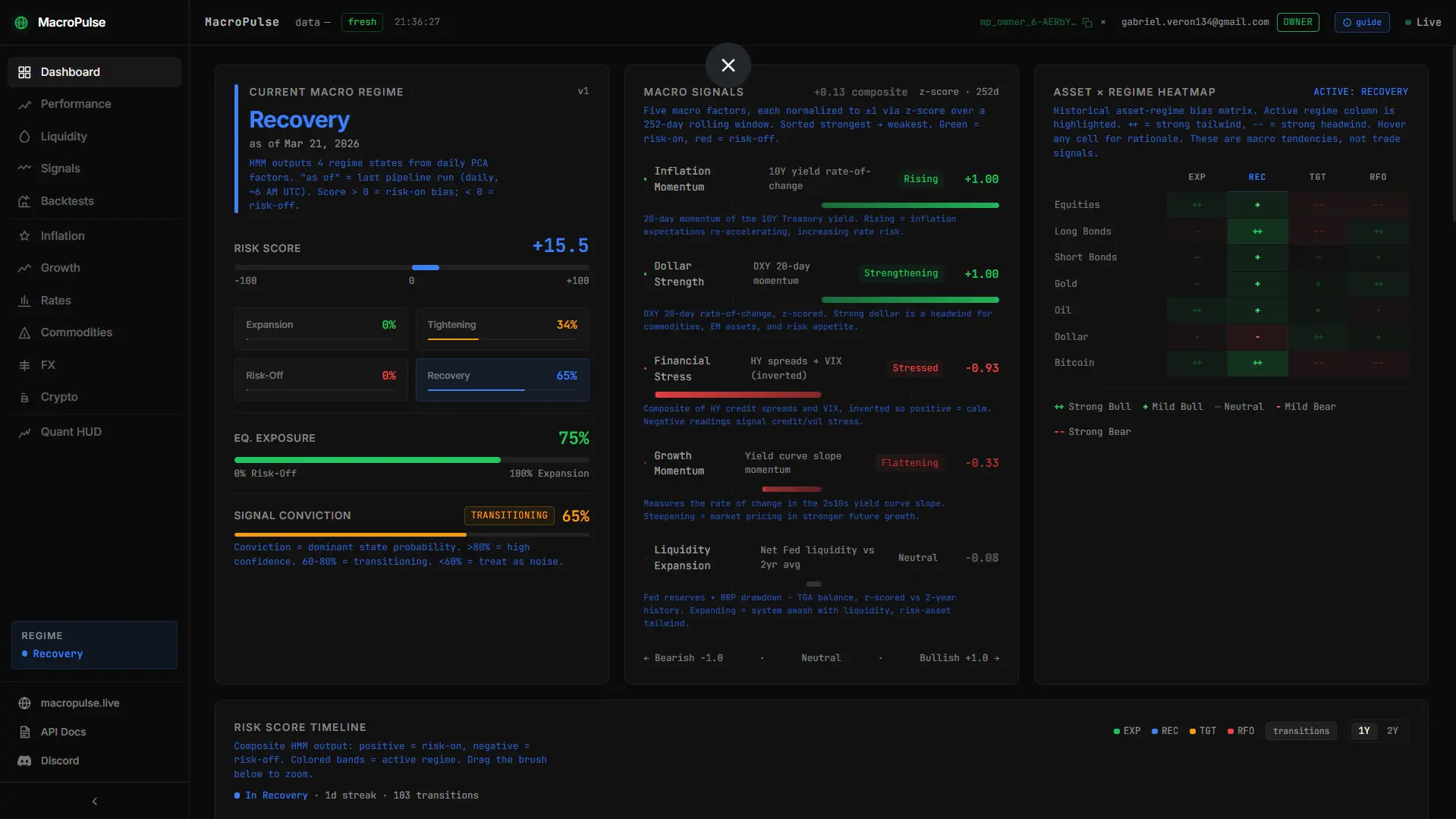

MacroPulse is a high-fidelity API-first infrastructure designed for quant traders and fintech developers. It leverages Hidden Markov Models (HMM) and Principal Component Analysis (PCA) to denoise fragmented global data into machine-readable macro-regime signals. By delivering Alpha-as-a-Service, MacroPulse eliminates the cognitive load of manual data synthesis, providing the systemic layer required for automated execution and macro-risk management.

Screenshots

Reviews (0)

No reviews yet. Be the first to rate this product!

Comments (2)

Machine-readable macro alpha via API using PCA and HMM modeling is niche but powerful for quant teams. MacroPulse brings institutional-grade signals to systematic traders.

Macro-discretionary trading is traditionally plagued by noise and cognitive bias. We built MacroPulse to serve as the connective tissue between fragmented data and executable strategy.